Getting ready for retirement in 2023 means understanding the intricacies of Medicare registration. Overlooking your enrollment period could lead to penalties for late applications.

Besides pinpointing the right time to sign up, it’s equally important to be aware of the anticipated Medicare costs and the kind of coverage essential for your needs. But before diving deeper, may I ask at what age you’re planning to retire in 2023?

“Set to Retire at 65 in 2023?”

If you’re eyeing retirement at 65, you’ll need to register for Medicare during your Initial Enrollment Period (IEP). This period spans seven months, starting three months before you turn 65 and concluding three months after your birthday. If you enroll prior to your 65th birthday month, your Medicare benefits will commence on the first day of that month. However, if you register in the three months following your 65th birthday, your coverage will kick off on the first day of the subsequent month.

Typically, employer-provided insurance remains active until the month’s end, when you retire. However, this can differ based on the employer, so it’s wise to touch base with your HR team to ascertain the exact termination date of your workplace insurance.

What to do If You Retire Before 65

If you’re looking to retire before hitting 65 and won’t retain insurance from your former employer, you might want to think about opting for an ACA plan. You can explore available plans in your vicinity on healthcare.gov and select one that aligns with your budget.

It’s essential to note that ACA plans don’t count as creditable coverage for Medicare. Hence, when you approach 65, it’s advisable to shift to Medicare. Ensure you register for Medicare within the 7-month IEP timeframe. Subsequently, delve into Medigap or Medicare Advantage plans to determine which aligns best with your requirements. After finalizing your Medicare coverage, reach out to your ACA provider to terminate the plan. Ideally, you can arrange for your ACA coverage to conclude at the month’s end, with Medicare taking over at the start of the next month.

If you retire before 65 and opt for Cobra from your past employer, you should still enroll in Medicare during your IEP.

Are You Past 65 and Retiring in 2023?

If you’ve missed your IEP window but either you or your spouse are still actively employed with a large company, you’ll qualify for a Special Enrollment Period (SEP) to register for Medicare once that employer’s health coverage ceases. You’ll be granted an 8-month period to sign up for Medicare after losing such coverage or ending employment to avoid any penalties for late enrollment.

Yet, many opt to have their Medicare benefits kick in right after their previous employer-based coverage concludes. It’s advisable to initiate the Medicare application roughly two months before you want it to take effect, given that Social Security processing can span several weeks. When applying due to the loss of creditable coverage, ensure you provide both CMS Form 40B and CMS Form L564 to the Social Security office.

For those considering employment with a smaller firm post-65, it’s crucial to understand that Medicare will be the primary coverage, with the group plan acting as secondary. Hence, it’s wise to enroll in Medicare during your IEP to sidestep any penalties for delayed enrollment.

Retiree Coverage

Should you be presented with Cobra or retiree insurance upon retirement, it’s typically beneficial to activate Medicare immediately when transitioning to Cobra or the retiree scheme. These alternatives often act as supplements to Medicare Parts A and B. To get clarity on how your retiree insurance integrates with Medicare, it’s best to liaise with your HR team or directly reach out to Medicare.

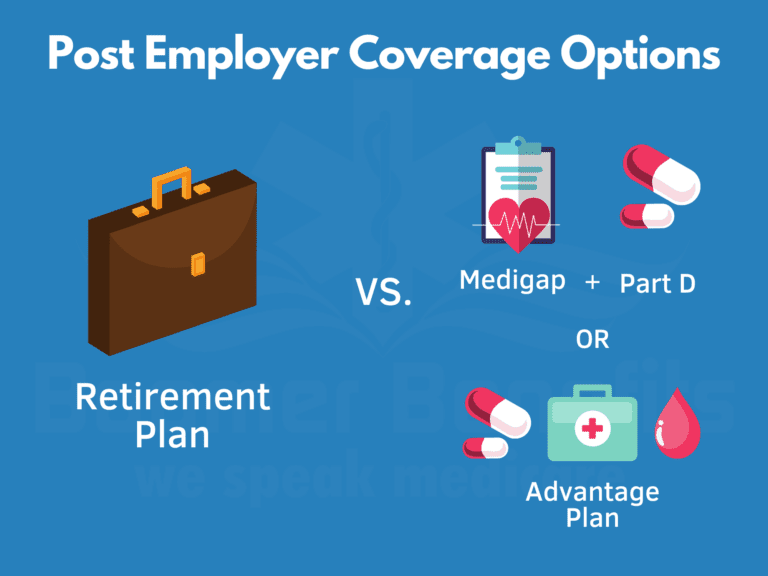

Post-Employer Coverage to Consider with Medicare

If your previous employer provides you with a retiree plan option, it’s worthwhile to juxtapose that with plans from private insurers, like Medicare Advantage or Medicare Supplement plans. Often, these private plans might offer more financial advantages compared to the retiree plan.

Medicare doesn’t shoulder the entirety of your hospital and medical service costs. Anticipate some shared expenses, including copays, deductibles, and a 20% coinsurance for services, without a ceiling on these charges. This shared cost aspect underscores the rationale behind many opting for supplemental insurance.

Medicare Supplement Option

A Medicare Supplement Plan, often referred to as Medigap acts as a secondary plan to assist in covering those additional expenses. Its primary function is to address costs after Medicare has made its payment, aiding in managing deductibles, copays, and coinsurance. Upon the activation of your Part B, a 6-month Medigap Open Enrollment period commences, during which you can join a Medigap plan without undergoing any health-related inquiries. However, after this period, in several states, you might be required to respond to health-related questions.

Prescription Drug Plan

Furthermore, it’s advisable to sign up for a Part D prescription plan to secure outpatient drug coverage. If you register for Medicare during your IEP, you should also join a Part D plan within that same seven-month timeframe. Some individuals might opt to enroll at a later stage, post their IEP, especially if they continue working beyond 65 and their workplace insurance caters to their medication needs. In such cases, a 2-month Special Election Period is granted from the day the employer-provided coverage ceases, allowing enrollment into a Part D plan.

Medicare Advantage Option

Another avenue to consider is the Advantage plan, which serves as an alternate method to avail your Medicare benefits. This plan comes into play for hospital visits or any medical service requirements. Advantage plans might extend coverage for services not encompassed by Medicare, like regular dental, vision, and hearing care, and can also incorporate drug coverage.

The registration periods align with those of Part D. If you’re initiating Medicare at 65 upon retirement, you can enroll during the same seven-month span. But, if retirement comes post-65, a two-month timeframe is available for Medicare Advantage plan sign-up. Should you overlook this period, you’d need to await the subsequent enrollment opportunity, like the Annual Election Period that rolls around each autumn.

Medicare Costs You Need to Know Before Retiring in 2023

The majority of individuals don’t pay a monthly fee for Medicare Part A, given they’ve worked a minimum of 40 quarters within the U.S. If you haven’t met this 40-quarter criterion, the premium could be either $278 or $506, contingent on the number of quarters worked. Eligibility for complimentary Part A can also be achieved through a spouse aged 62 or older, provided you’ve been wed for at least a year. Even an ex-spouse’s or deceased spouse’s work record can grant you this benefit, so most don’t bear the cost for Part A.

Conversely, every Medicare recipient is obligated to cover the Part B premium. For 2023, the standard foundational premium stands at $164.90. Certain individuals might incur a higher Part B fee, influenced by their earnings.

Social Security assesses your tax documentation from two years prior. If, in 2021, your MAGI exceeded $97K as an individual or $194K jointly, your 2023 fee will be higher. The surplus you remit beyond the foundational premium is termed the Income Related Monthly Adjustment Amount (IRMAA). Should there be alterations in your income, you have the option to contest the IRMAA. Annually, Social Security revisits your Part B premium, notifying you of any changes for the forthcoming year via a Benefit Determination Letter, typically dispatched in December or January.

Beyond the premiums for Original Medicare, it’s prudent to gauge the potential costs of a Medicare Advantage plan, Medicare Supplement plan, and Part D plan as you approach retirement in 2023, ensuring a smoother transition.

Final Point

Preparing for retirement requires meticulous attention, given the various enrollment periods to monitor and understand. Moreover, it’s essential to be clear on your financial limits and evaluate all available choices, ensuring you select the most economical solution tailored to your needs.

Many eagerly anticipate retirement, and our primary goal is to facilitate a seamless shift for our clients into Medicare. Our proficiency in Medicare registrations and plan options sets us apart. If 2023 marks your retirement year and you seek guidance exploring your alternatives, don’t hesitate to reach out. Our assistance comes at no cost to you.

Key Takeaways

- In 2023, consider registering for Medicare if retiring before age 65.

- Use the designated Initial Enrollment Period for Medicare registration.

- For those retiring after age 65, two specific forms need to be completed.

- Submit the completed forms to Social Security.

- If provided with retiree benefits, evaluate them.

- Compare retiree benefits to Medicare Supplement or Medicare Advantage plans.